-

September 16, 2019

-

What American food retailers can learn from China’s push to integrate e-commerce mobile technology into existing brick-and-mortars. A smartphone becomes a magic wand in the hands of shoppers inside two new Chinese supermarkets owned by e-commerce giants Alibaba and JD.com.

Using a mobile app, shoppers can scan a barcode on any vegetable for recipe ideas and learn exactly where it came from and when it arrived in the store. They can order prepared dinners to take home. They can shop the supermarkets’ online sites while perusing the aisles and have those items delivered to their homes within 30 minutes. And when they’re ready to check out, they can do so without the aid of a cashier.

All these convenience features generate gold for Alibaba and JD.com. The harvested information provides critical data on inventory and shopping preferences and facilitates micro-targeting of promotions to individual shoppers.

Welcome to the Future of Grocery Shopping

Like retailers the world over, Chinese merchants are experimenting with ways to increase the appeal of the physical shopping experience to entice and retain customers. Within the convenience food and grocery sector, rivals Alibaba and JD.com are reinventing the supermarket by seamlessly integrating e-commerce mobile technology into existing brick-and-mortar locations.

Alibaba touts its “Hema” model as “new retail” that melds together online and offline shopping, thus erasing the line that has traditionally separated the two. JD.com describes “7Fresh” as “boundaryless retail” — a crossover between online, offline, and virtual shopping. Both retailers opened flagships in Beijing within the past three years and have since rolled out stores to multiple locations across the country with plans for more.

Though new, the arrival of these revolutionary emporiums can, in fact, be traced back over the past decade to a number of factors that developed within China. Indeed, these factors make China a veritable laboratory for defining the sweet spot between physical shopping and digital advancement. The world is watching.

The Smartphone Changed Everything

China’s is the largest mobile market on the planet. Thanks to the combination of an expanding middle class and a government push to build out the digital infrastructure, China boasts 800 million internet users (versus 300 million in the United States). Of these, a remarkable 98 percent access the internet through their phones.

That enormous demand has helped quickly advance mobile offerings and agile solutions for consumers who value speed and convenience. Online music, video streaming, live streaming, and social media-sharing are deeply woven into the fabric of society.

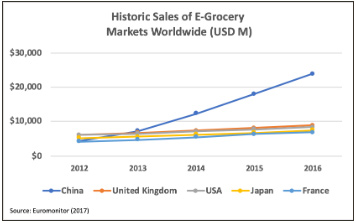

The trend extends to online food ordering or e-grocery. Between 2012-2016, e-grocery in China showed a compound annual growth rate (CAGR) of 53 percent, representing 33 percent of the market share. (By contrast, e-grocery sales in the United States grew at a CAGR of only 8 percent during the same period, representing just an 11 percent share.)

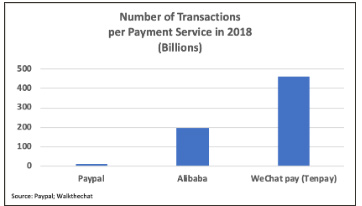

Payment systems have followed suit. Because relatively few Chinese consumers hold credit or debit cards and banks are considered bureaucratic, digital banking has taken off. Mobile apps such as Alipay (owned by Alibaba) and WeChat Pay (owned by Tencent which also owns a stake in JD.com) each handle more payments in a single month than PayPal does in an entire year. By 2021, eMarketer predicts that 80 percent of smartphone users in China will be using their phones at point-of-sale checkouts, compared to only 31 percent of smartphone users in the United States and 22 percent in Germany.

Both Alipay and WeChat Pay exist in unique ecosystems that integrate social media, e-commerce, and payment options into a convenient, one-stop, user-friendly interface that is the height of convenience for retail integration. According to the PwC 2017 Total Retail Survey, 52 percent of Chinese online shoppers use their mobile phone on a weekly basis to make purchases. Only 14 percent of global online users do the same.

Innovation Nation

Could the complete digitization of commerce be the key to saving physical retail? It might be said that China’s brick-and-mortar food sector is putting that theory to the test.

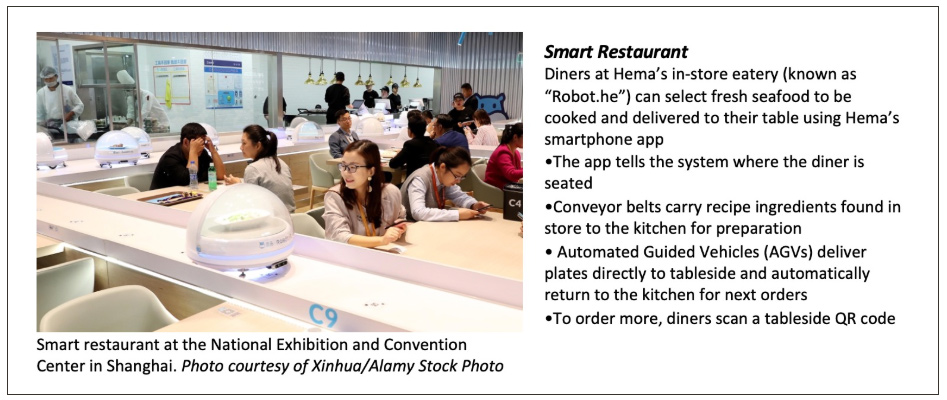

At Hema, shoppers are enticed to try new imported options through clean, eye-catching displays. In addition to identifying the origin of items, barcodes provide suggested recipes using ingredients found around the store. Every Hema is intended to be a local resource; employees fulfill online orders by picking up items and placing them on a conveyor belt to meet a guaranteed free 30-minute delivery time to customers within a 3-kilometer radius.

Meanwhile, technology at the higher-end 7Fresh is a dazzling step ahead of Hema. Magic mirror screens throughout stores link with an app to display nutritional and product history. Autonomous shopping carts follow behind shoppers as they stroll the aisles.

In JD.com’s “unmanned” stores (called JD.ID X), artificial intelligence drives convenience: scanners identify shoppers as they enter through facial recognition. At checkout, a terminal confirms identity and charges the shopper's store credit card for items collected. For retailers, the bonus is a reduction in labor expense and tight inventory tracking.

The trend is even extending down to the mom-and-pop level to help traditional, community-based stores remain competitive and useful. Alibaba offers these legacy players a customized mobile app to better track inventory, improve logistics and facilitate reordering of items, rather than having to rely on owner intuition. The focus is on region-specific items, and owners can order from a single distribution center instead of multiple sources, thus facilitating shelf restocking in as little as one day.

Imagine if a Walmart or Costco offered a similar small business-focused analytics suite and distribution package in the United States. Might it be a difference-maker for the little guys? We may be getting a preview right now from Amazon’s highly successful push into the B2B space with its four-year-old Amazon Business. Though it has not yet reached out to small family businesses, the platform’s model of efficiency and supply is making quick inroads with larger retailers.

American Ingenuity

The U.S. mobile infrastructure is not nearly as extensive as it is in China. Still, U.S. retailers with an experimental mindset might try adapting some of the various facets of digital technology that are available here into their brick-and-mortars. By incorporating digital shopping applications and payment systems (e.g., Apple Pay) based in cloud commerce, for instance, retailers can not only streamline the shopping experience but also gain the benefits of big data analytics.

Already, Target and Walmart have upgraded digital offerings to better bridge the online-offline shopping experience. But way ahead of those retailers is the Amazon Go convenience store, now in 13 locations nationwide. Like JD.ID X, Amazon Go relies on artificial intelligence to facilitate “scan-and-go” shopping — that is, the ability to pick up items and walk out without interacting with a cashier. Entire families can scan into the store upon entry using the parent’s Amazon Go app, which allows each member to shop separately on the parental account.

Overcoming Cultural Hurdles

Beyond technological challenges, there are a few cultural hurdles in the United States that account for slower adoption of e-grocery compared with China.

For one, companies have less of an incentive to innovate, since the U.S. primary family shopper is not as hard-pressed for time as her Chinese counterpart. Perhaps the demand for speedy online grocery delivery is not as great here.

Furthermore, U.S. shoppers prefer to pick out their own produce rather than trusting someone else to do it. Finally, U.S. shoppers tend to view the grocery store as a repository for replenishing necessities at home, not as a place to discover global variety or experience new regional cuisine.

But then again, the most successful and disruptive offerings give consumers what they didn’t think they needed or wanted. U.S. food merchants should consider taking a low-tech page from the Chinese model to enhance the physical shopping experience right now. Providing more experiential food options, for example, such as in-store cafes or take-out prep, adds convenience. And ramping up global offerings and offering a wider variety of brands to choose from might stimulate impulse buying.

Across the industry, digital technology is transforming every aspect of our lives. The advancements in the convenience food and grocery sector emanating out of the East spells change for the way we shop for what we eat in the West. The question is, how, and when, will American grocery stores transform in the digital age?

© Copyright 2019. The views expressed herein are those of the authors and do not necessarily represent the views of FTI Consulting, Inc. or its other professionals.

About The Journal

The FTI Journal publication offers deep and engaging insights to contextualize the issues that matter, and explores topics that will impact the risks your business faces and its reputation.

Related Insights

Published

September 16, 2019

Key Contacts

Key Contacts

Consultant