-

October 15, 2018

-

FTI Consulting’s survey of 100 top retailers revealed some hopeful news.

For all the gloom and doom about the state of retail, some bright spots have emerged in the wake of aggressive initiatives begun by top retailers over the past two years. These initiatives offer a sense of optimism for the future, though great uncertainty remains.

FTI Consulting’s survey of 100 top retailers revealed some hopeful news.

For all the gloom and doom about the state of retail, some bright spots have emerged in the wake of aggressive initiatives begun by top retailers over the past two years. These initiatives offer a sense of optimism for the future, though great uncertainty remains.

That conclusion is borne out in findings from FTI Consulting’s 2018 Retail Executive Survey. Following several years of stagnant-to-modest sales growth, margin pressure and industry fragmentation, FTI Consulting was curious to understand how executives were rising to meet industry challenges. The survey reached 100 executives, including CEOs, COOs and strategy officers, and covered a range of topics, including anticipated industry changes and strategic initiatives.

It turns out that store-based retailers are making slow and steady progress tackling key issues. This continues a trend from FTI Consulting’s 2017 survey.

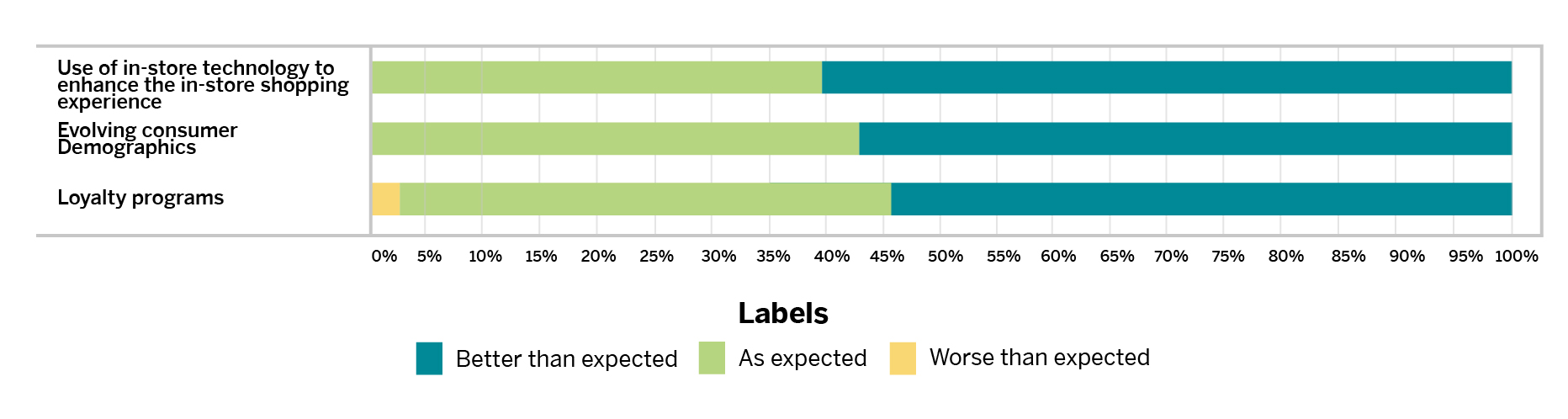

Better-Than-Expected Results

In both the 2017 and 2018 surveys, FTI asked the executives about initiatives they are taking to address key industry challenges (“categories”), such as changing consumer demographics and intensely competitive pricing. In 28 of the 29 categories, more than 50 percent confirmed they had either already begun an initiative within the past two years, or have plans to do so in the coming year.

The 2018 survey showed some of the positive effects of these efforts: Most executives reported that completed projects yielded results either as expected, or better than expected. In three initiatives (shown below) the results were better than expected more than 50 percent of the time.

Given the pervasive reports about the “death” of in-store shopping, this result may appear surprising. But as FTI reported in an earlier article, “No, the Sky is Not Falling: Why the Business Media Needs to Refresh the Narrative About Retail,” there are numerous misperceptions about the state of retail today.

Competing with Amazon

The long-held convention about Amazon is that it poses a business threat to most large retailers. Survey respondents did not veer far from that line, but a related response produced a noteworthy result.

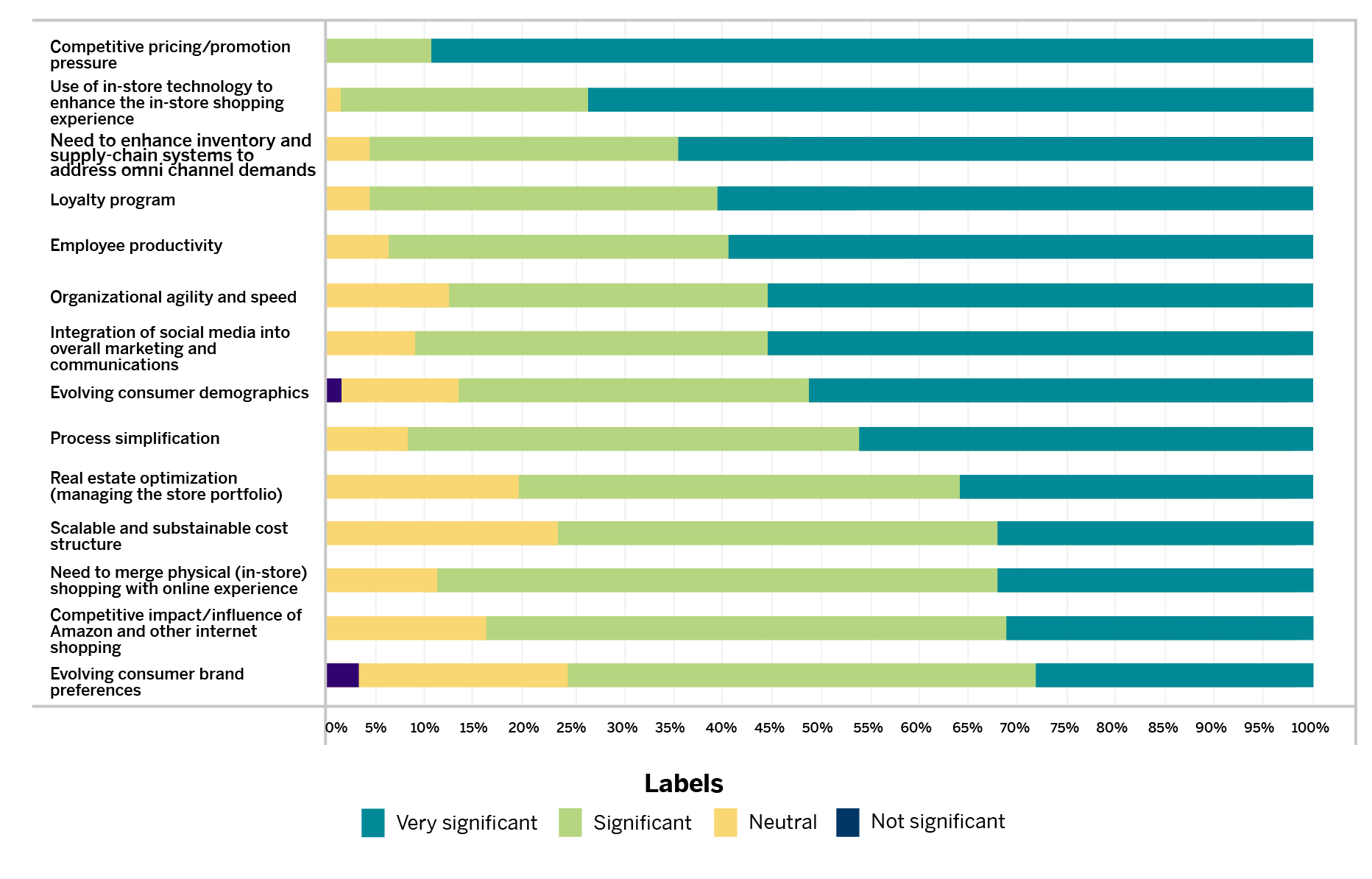

When asked to rank the 14 potential impacts to the industry in the next one to two years, only 32 percent rated the Amazon threat as being “very significant.” That placed it one spot from the bottom of all potential impacts ranked as “very significant” by the executives.

Note: The overall ranking of the Amazon threat was partially dependent on results of individual segments surveyed (e.g., 47 percent of big-box retailers ranked the threat as “very significant.”)

This is in line with FTI Consulting’s broader view on Amazon’s disruptive effects. In an October 2017 article, “Is Amazon Invincible?,” FTI noted that although Amazon is a clear leader in the online channel, its market share of total sales in many product categories is relatively small.

Further, the FTI article posited that upcoming retail bankruptcies “may have less to do with Amazon and the online shift than with strategic missteps or operational blunders [by retailers].”

It’s quite likely, however, that the response by retailers may also have to do with the fact that most now have their own online platforms by which they can reach customers who shop exclusively online or those who make purchases both in-store and online.

Closing the Capabilities Gap

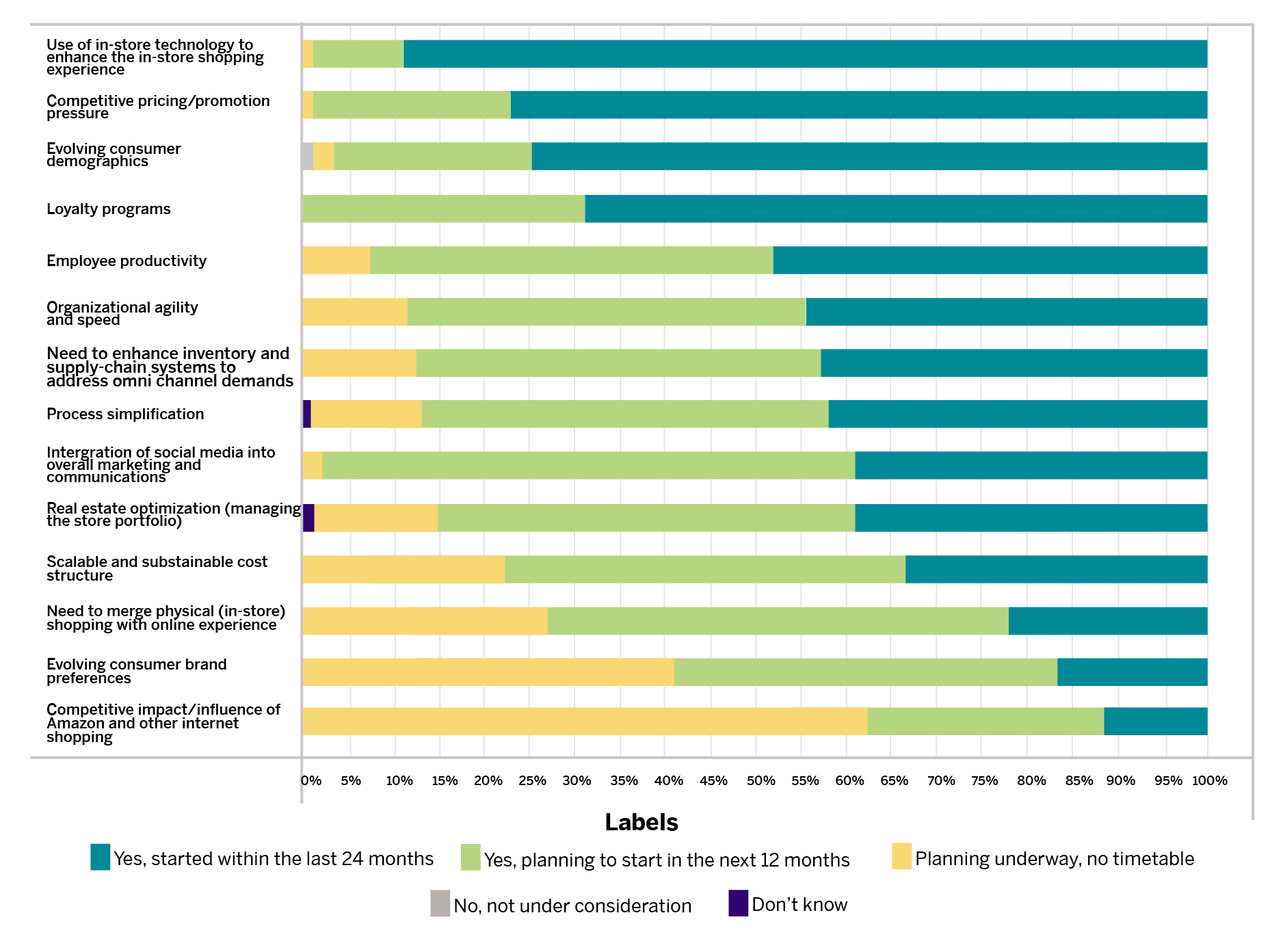

As seen in the graph above, in-store technology, competitive pricing and enhancing inventory and supply chain were the top three concerns among the 14 ranked by the retailers. However, the survey results indicated that retailers are taking action to address the first two weaknesses. As shown in the results below, more than 75 percent of respondents had started plans within the past two years to tackle those issues.

Addressing the third weakness — enhancing inventory and supply chain — fell much lower on the chart below. And yet it was high on the executives’ action plan: Almost 60 percent of respondents were planning to address this concern in the coming year.

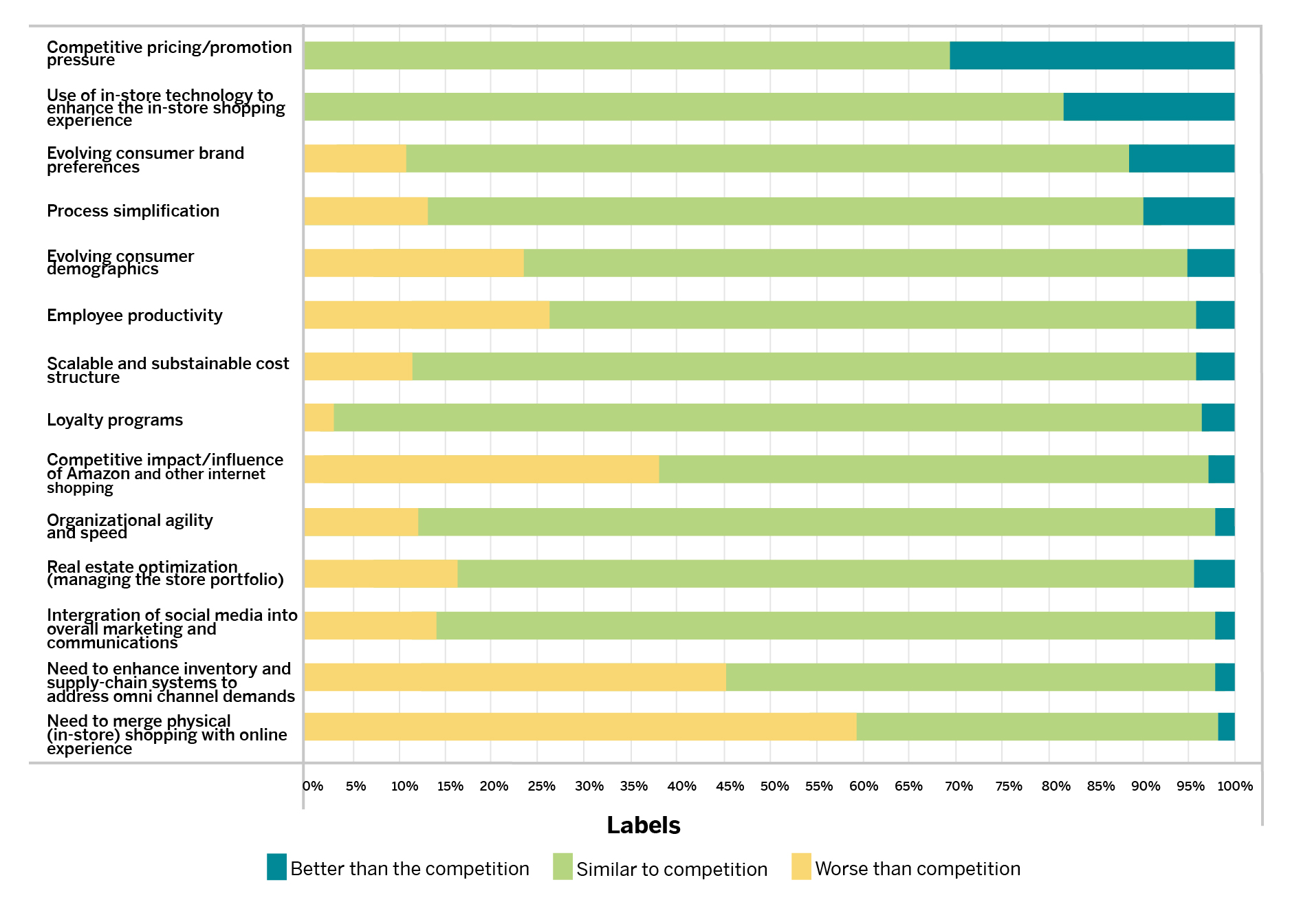

Keeping Up with the Competition

When it came to the top concern of competitive pricing and promotion pressure, respondents seemed especially confident in their abilities. Of those who said they have plans to address the issue, 30 percent indicated they are better at this than their competitors.

Overall, the vast majority of respondents rated all their abilities as “similar” to the competition. However, more than half (59 percent) ranked themselves behind their competitors in merging physical shopping (in-store) with an online experience — the vaunted omnichannel option.

What does this mean? Only that retailers may simply not have a blueprint for action.

Going All Out with Omnichannel

Today’s fragmented retail industry demands an all-out approach to appeal to consumers however they shop.

To that point, some of the original retail disruptors — online merchants — have developed a new tact: opening brick-and-mortar locations. The move shows promise. According to The Atlantic, more than half of all sales at Warby Parker, once an online-only retailer of prescription sunglasses and glasses, occurred in a physical store. Similarly, the men’s online apparel brand Bonobos has opened 51 “showrooms” throughout the country where customers can schedule an appointment to be measured and sample merchandise before ordering through its website.

Even Amazon has entered the physical retail market. The Seattle-based giant acquired Whole Foods in 2017, launched several Amazon Go stores, opened 13 bookstores and is partnering with Kohl’s to handle some of its product returns.

Elsewhere, some retailers have turned to an old-school strategy for reaching customers that was once thought dead in the digital age: the mail order catalogue. This option provides retailers with the opportunity to tell their brand story in their own way, to differentiate themselves and sustain customer relationships. One example is the women’s clothing and accessories brand Anthropologie which refers to its catalog as a “journal,” claiming that it represents an opportunity to “inspire and engage.”

Conclusion

The reality of the in-store retail industry is that it must continue to tackle the omnichannel challenge to remain relevant. Many stores have started to address this on the back end by reorganizing supply chains, expediting online orders and improving the returns process.

Retailers that continue to meet the myriad demands of customers and enhance their brand through unique ideas and aggressive innovation will be best positioned for a brighter future.

About The Journal

The FTI Journal publication offers deep and engaging insights to contextualize the issues that matter, and explores topics that will impact the risks your business faces and its reputation.

Published

October 15, 2018

Key Contacts

Key Contacts

Managing Director